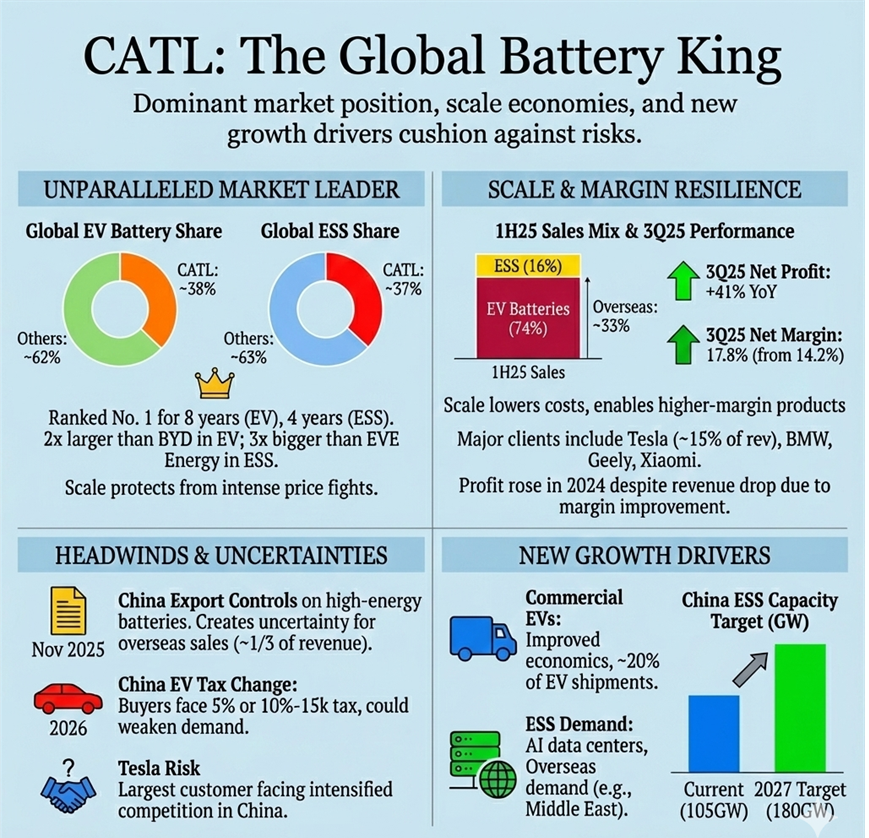

Contemporary Amperex Technology (CATL, 3750 HK) is the world’s biggest maker of batteries for electric vehicles (EVs) and energy storage systems (ESS). Its size in both markets gives it clear advantages and makes it hard for rivals to catch up.

Unparalleled market leader

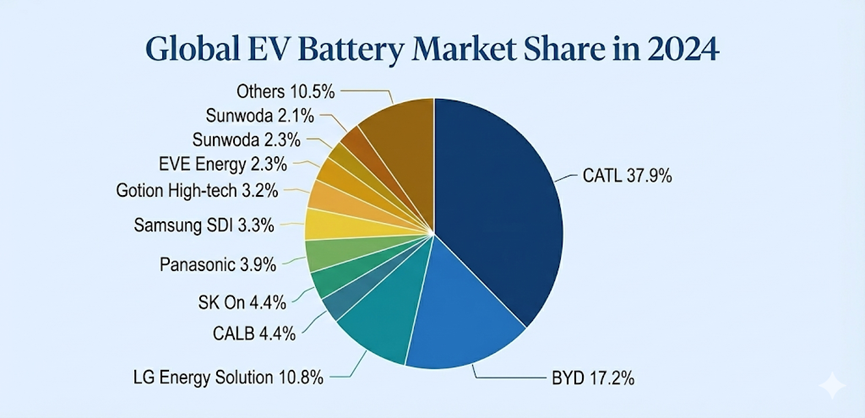

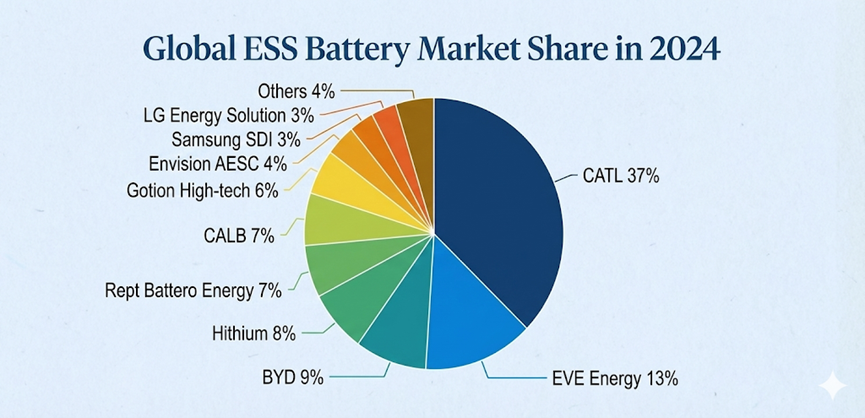

CATL holds around 38% of the global EV battery market and about 37% of the ESS market. In addition, it has been ranked No. 1 for 8 and 4 consecutive years in the global EV and ESS markets, respectively.

It is more than twice as large as BYD (1211 HK) in EV batteries and roughly three times bigger than EVE Energy (300014 CH) in ESS. Outside the big players, the market is split among many smaller firms, which helps protect CATL from intense price fights.

That scale lowers costs—for buying raw materials and for making batteries—and lets CATL push higher‑margin products. Its customers include major global carmakers such as Tesla (largest customer, about 15% of revenue in 2024), BMW, Mercedes‑Benz, Volkswagen, and Stellantis, as well as Chinese brands like Geely, Li Auto, and Xiaomi. In the first half of 2025, about 74% of sales came from EV batteries and 16% from energy storage, and roughly one‑third of revenue was from overseas—a meaningful degree of geographic diversification.

China’s midstream dominance fuels CATL’s battery edge

CATL’s competitive edge is not just about design or manufacturing scale—it is also reinforced by China’s near‑dominance of the midstream processing that turns mined ore into battery‑grade chemicals and components. Currently, China accounts for roughly 65%–95% of the global midstream processing capacity for five key EV‑battery raw materials—lithium, nickel, cobalt, graphite, and manganese. The access to competitively priced, reliably processed raw materials helps CATL to lower costs, shorten lead times, and lock in supply for new plants and long‑term OEM contracts.

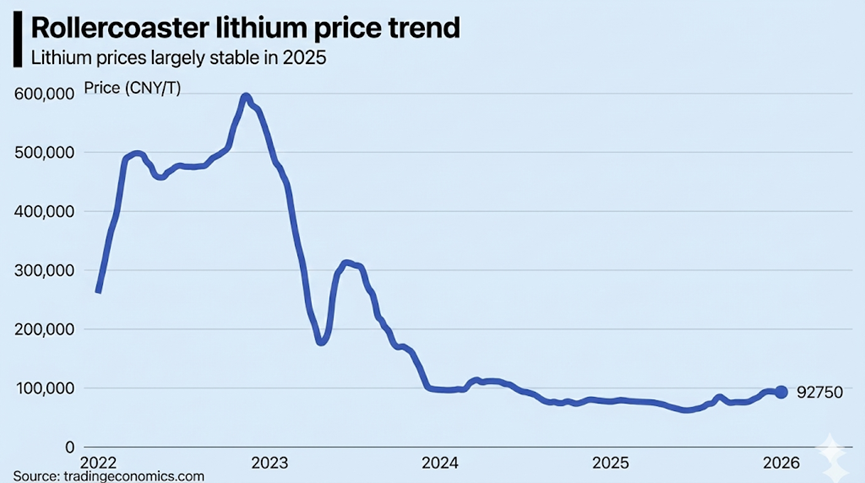

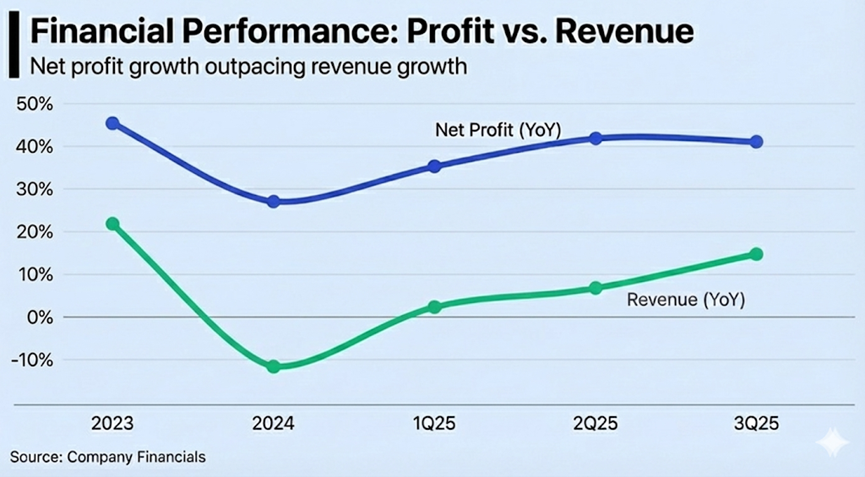

How CATL handled the lithium rollercoaster

Lithium prices surged in 2021–22 and then fell as new supply arrived. That swing hit revenues: CATL saw roughly a 10% revenue drop in 2024 despite a 22% rise in shipments. But profit still rose (about 16%) because margins improved—economies of scale and a better product mix helped offset lower prices. In the first nine months of 2025, steadier lithium prices supported about 9% revenue growth and a 36% jump in profit as margins kept improving.

The 3Q25 numbers make the point. Sales were up 13% year‑on‑year and net profit climbed 41%, lifting net margin to 17.8% from 14.2% a year earlier. In other words: when commodity turbulence eases, CATL’s economics accelerate quickly.

Trends to watch

- Policy change: From 2026 China will cut the EV purchase tax cap in half. Buyers will face a 5% tax for EVs priced below CNY300k or a 10% tax minus CNY15k for EVs priced above CNY300k, which could weaken demand. How pronounced that slowing might be will depend on price elasticity and how quickly automakers adjust.

- Customer risk: Tesla, CATL’s largest customer, has been facing intensified competition in China lately. On a positive note, CATL could mitigate this via market share gains from other domestic OEMs given its broad customer base. For example, Xiaomi, another major client for CATL, has been gaining traction lately.

- Export rules and geopolitics: China introduced export controls on very high‑energy batteries in November 2025. That creates uncertainty for overseas sales (about a third of CATL’s revenue). The impact depends on trade talks and how quickly CATL expands production outside China, such as in Hungary and Spain.

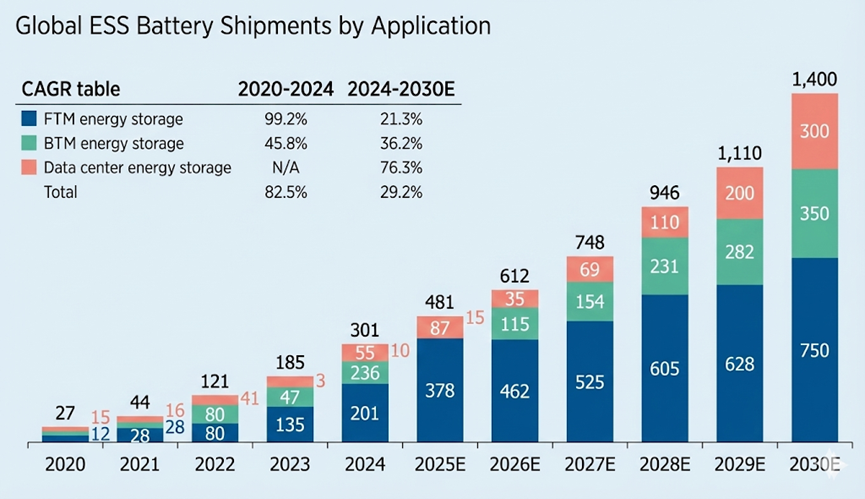

- Commercial EVs and energy storage could be new drivers. Lower battery prices in recent years have led to improved economics of commercial EVs, which account for about 20% of CATL’s EV battery shipments. In the energy storage market, future demand is supported by 1) AI data centres; 2) The Chinese Government’s plan to increase new energy storage to 180GW by 2027 versus about 105GW currently; 3) Overseas market demand especially in the Middle East.

The global energy‑storage system (ESS) market is set for rapid expansion, with shipments forecast to soar from about 250GWh in 2024 to roughly 1,400GWh by 2030 (c.29% CAGR). The market is segmented into front‑of‑the‑meter (utility and grid), behind‑the‑meter (industrial, commercial, and residential), and data‑centre storage, and the fastest‑growing slice will be data‑centre batteries — projected to expand at roughly a 76% CAGR through 2030—driven by massive cloud and AI demand.

Easing of capacity constraint to boost volume

Management admits that temporary capacity constraints have cost market share. The pipeline of new capacity due to come online in 2026 should ease those bottlenecks and allow CATL to convert demand into volume more readily.

Share stabilised after expiry of H-share cornerstone lock-up

CATL is listed in both Shanghai and Hong Kong. CATL’s Hong Kong H‑share float is tiny (3.4%) relative to its overall market capitalisation, due to a light H‑share issuance at the recent IPO and large cornerstone allocations (50%). With half of those H‑shares subject to a six‑month lock‑up that expired on 19 November 2025, the counter experienced some post‑expiry volatility; the subsequent stabilisation suggests markets are digesting the potential supply risk.

Bottom line

CATL’s size gives it real advantages: lower costs, strong customer relationships, and the ability to sail through the commodity cycles. Risks from policy and geopolitics exist, but overall CATL looks well placed to benefit from the global shift to electrification.

This article is for information only and is not investment advice or a solicitation to buy or sell securities. This article does not constitute a “Personal Recommendation” or investment advice under UK FCA regulations. The author holds NO position in the securities mentioned. There is no warranty as to completeness or correctness. Please do your own due diligence or consult a licensed financial adviser. Investing in Asian markets involves significant risk. Please read the Full Disclaimer before acting on any information. Images and videos created with the assistance of Gemini AI.

Latest posts